When most people think of wealth and how to create it, they think of income. But the secret about wealth is that what you earn is only half the battle. The other half rides on how you manage your money.

Trading and investing apps have already exploded in popularity, the gig and freelance economy continues to gather steam amidst the pandemic, and increasing numbers of Millenials, Gen Z’ers and young start-ups are turning towards platforms like Instagram, YouTube and Tiktok to market their products (or themselves). Younger generations are waking up to the fact that simple living and saving can maximise their funds for a much shorter working life – and new, accessible financial technology is helping them get there.

Traditional banks – tone deaf as ever to generational shifts – do not resonate with these growing groups. With 2020 seeing off the remainder of new account rewards, interest rates in the toilet, ATMs all but obsolete, and swathes of high-street bank branches shutting down, mobile-friendly banking alternatives like Monzo, Starling and First Direct are having their moment, creating a change in the way people are managing their money.

The Plum App: Facts & Figures

Plum’s timing has been shrewd. It launched in 2016, amidst ongoing volatility following the GFC of 2008. Between Christmas last year and summer 2020, it’s grown from 650,000 users to 1 million.

Plum’s corporate tagline reads, ‘the app that boosts your bank balance’, and it presents some pretty impressive figures for its users. It claims to have achieved £200 million plus, set aside by the 1 million users across the UK.

What Does Plum Actually Do?

Think of it as a savings robot. Plum uses AI to analyse your spending, and identify patterns and ways you can set money aside. It does this across a few different (and kind of quirky) functions:

The ‘Roundup’ tool: rounds up the price of all of your purchases to the nearest pound, allocating the difference to your virtual piggy bank.

Auto-deposit: every payday, you can instruct Plum to take a specified amount out of your wages to squirrel away (e.g. £100 a month).

The 52-week challenge: a fun little game where you put away £1 in the first week, £2 in the next, £3 the next, and so on. Be amazed by the cumulative amount.

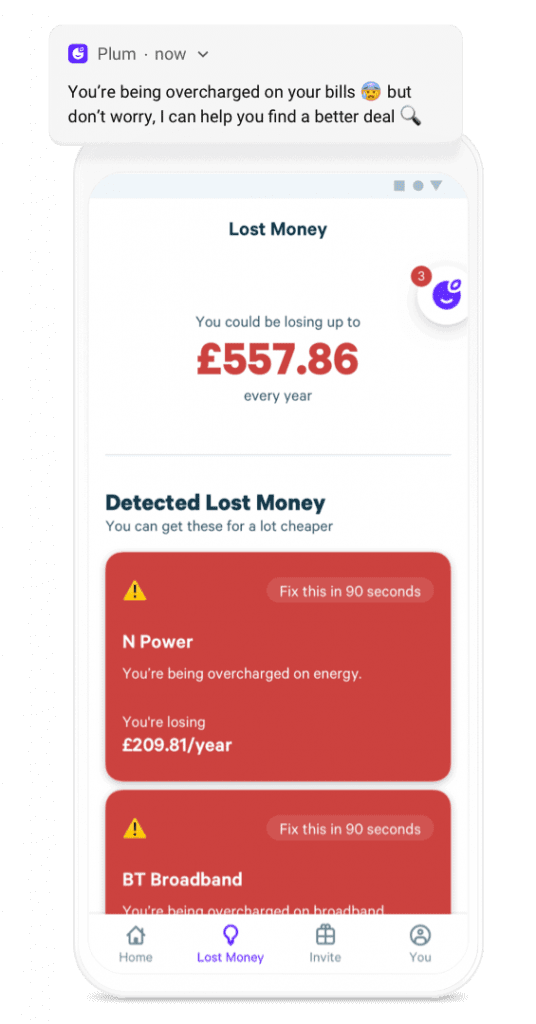

Lost Money: Another interesting feature Plum offers is automated bill switching. Plum will notify you if it thinks you’re paying too much for utilities, and help you transfer to a different provider. Seeing as an estimated 11 million households overpay for their electricity bills, resulting in a nationwide loss of £3.5 billion, this is a valuable function.

Is the Plum App Right For Me?

The bill-switching function is a perfect example of what Plum commodifies: not money, but time. Our financial health is often like a faint siren in the distance. We know certain changes could make us wealthier, but let’s face it – sitting down to review statements, compare providers and set up direct debits is boring. It requires not just time, but energy, patience and motivation. So we shuffle it to the bottom of our to-do lists and continue to overpay for the convenience of not addressing it. In that sense, we’re our own worst enemies.

Plum brings that siren screaming into our attention (in a nice way). And your attention is key in the psychology of why it works. Saving can feel like a pain point. It’s a long term reward – it gives us no instant gratification (in the way spending does). This is why so many people avoid it. Plum’s automated functions like the roundup tool allow you to set aside cash without noticing. This removes the pain from the process of putting money aside.

Another thing we conveniently choose to avoid is the amount that’s actually leaving our bank accounts. Do you know how much you spent last month? Last week? Yesterday, even? Plum forbids us from burying our heads in the sand. It counters the negative impact of your spending habits by alerting you to patterns, habits and unnecessary expenses you may not have noticed.

Prefer to Invest Instead?

Check out our comparison between Freetrade and Trading 212. Get a FREE STOCK when you sign up for each of these platforms.

If you are someone who knows you should be paying more attention to your financial health and trusts artificial intelligence to do it for you – Plum is probably right for you. If you’re still unsure, let’s weigh up the pros and cons of the app itself…

Pros And Cons Of The Plum App

Pros

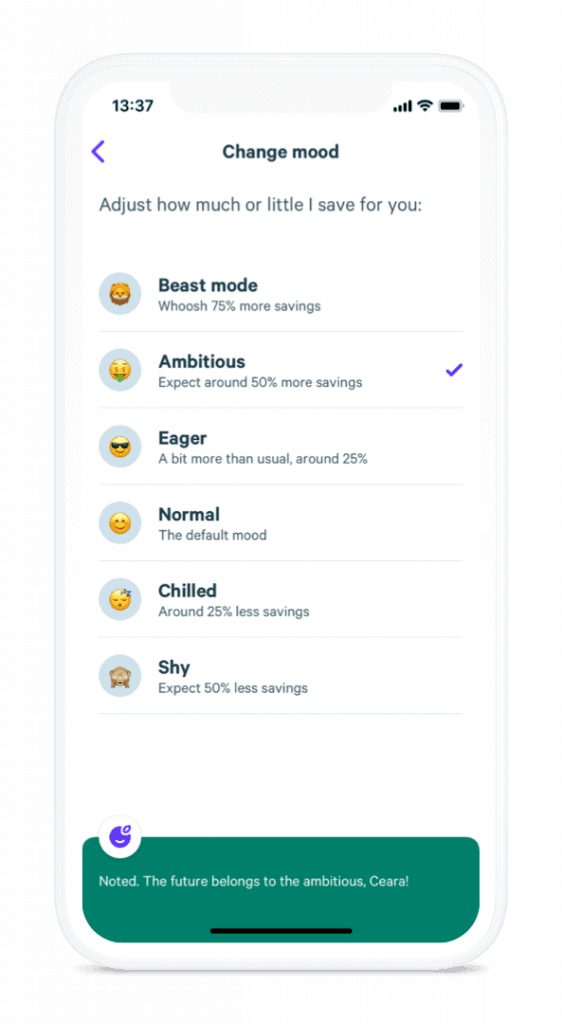

Plum lets you choose how aggressively you want it to put aside your money.

The algorithm adapts to your income and spending with 6 levels, from Chilled to Beast Mode, with varying impacts (i.e. Beast Mode will put aside 75% more than Normal mode, while Shy will put aside 50% less). This sense of variety really taps into the modern consumer’s desire for customisability. It also means Plum is not just for those needing help – whatever your speed, and whatever your budget, there’s a way to use Plum that will suit you.

Plum texts you updates – no need for constant checking.

In contrast to a lot of apps that keep you logging in all day every day, Plum sends you friendly reminders and emoji-laden notifications that advise you when it’s actioned a deposit for you

Plum uses a ring-fencing system to protect your money.

The less fintec-phobic among us might raise their eyebrows at the fact the free version of Plum does not offer FSCS protection (although the paid version does at £2.99, which offers a host of extra functions to help manage your money). But Plum doesn’t lend your money to any third parties – its e-money partner holds it as ‘e-money’. This money is protected by Electronic Money Regulations and you can apply to have it returned to you if Plum or their providers go bankrupt.

Cons

Plum doesn’t yet pay interest like a standard bank account.

If you elect to use the investing function, you may (keyword – may!) make a profit. But with the free Plum account, although you might be setting aside more money, you won’t be making any money on those funds. Interest rates on traditional savings accounts are currently pretty low, so this may not bother you, but you might be missing an opportunity if you’re stashing away larger volumes. If generating interest is important to you, there’s still an option – the Plum Pro version of the app (£2.99 per month) gives you access to an Easy Access interest-bearing pocket.

You can’t pop into a high street branch.

If you experience a technical issue with Plum, you have to go through a chatbot to speak to someone. Although it does have a customer service team working standard business hours, many people will be used to being able to speak face to face with bank advisers about transfers and withdrawals. Just remember – Plum is not a bank, and it doesn’t work like one. It’s a tool for money management, and it’s all online-only.

As with anything, it pays to start small and build up. Try downloading the Plum app and starting on Default or even Shy mode. It’s always very pleasing to see your change building up, and especially useful if you have a goal to set money aside for, like a holiday or a new car. The more you get to know the app, the more you might get to love the idea of a personal money-managing robot. The future is now.

Sign Up to Plum Today!

Start putting money aside and unlock potential Lost Money with Plum’s smart AI!

{kind=link}